Fixed vs. Variable Rate Mortgages in New Brunswick

Choosing the Right Mortgage Rate: What You Need to Know

One of the most important decisions you'll make when getting a mortgage is choosing between a fixed rate and a variable rate. Each option has advantages and disadvantages, and the right choice depends on your financial situation, comfort level with risk, and how you plan to manage your budget.

At New Brunswick Mortgage Matters, we help homeowners understand their options so they can make confident decisions. Here's what you need to know about fixed and variable rate mortgages.

What Is a Fixed Rate Mortgage?

With a fixed rate mortgage, your interest rate stays the same for the entire term of your mortgage. This means your payments remain consistent month after month.

Advantages of Fixed Rate Mortgages

Predictable payments make budgeting easier

Protection from rate increases during your term

Stability knowing exactly what you'll pay each month

Peace of mind if interest rates rise in the market

Disadvantages of Fixed Rate Mortgages

Higher rates compared to variable rates in many market conditions

Potential to pay more over the life of your mortgage if rates stay low or drop

Higher penalties if you need to break your mortgage early

A fixed rate mortgage is often a good choice if you prefer certainty in your budget and want to avoid any surprises in your monthly payments.

What Is a Variable Rate Mortgage?

With a variable rate mortgage, your interest rate moves up or down based on the market interest rate, also called the "prime rate." Depending on your lender and mortgage terms, either your payment amount will change or the portion of your payment going toward interest will change.

Advantages of Variable Rate Mortgages

Lower rates in many market conditions compared to fixed rates

Potential savings over the life of your mortgage

Lower penalties if you need to break your mortgage early

Historical performance shows variable rates often cost less over time

Disadvantages of Variable Rate Mortgages

Uncertainty about future payments if rates rise

Budgeting challenges when payments fluctuate

Potential stress during periods of rising interest rates

A variable rate mortgage may be a good choice if you're comfortable with some uncertainty and want to take advantage of potentially lower rates.

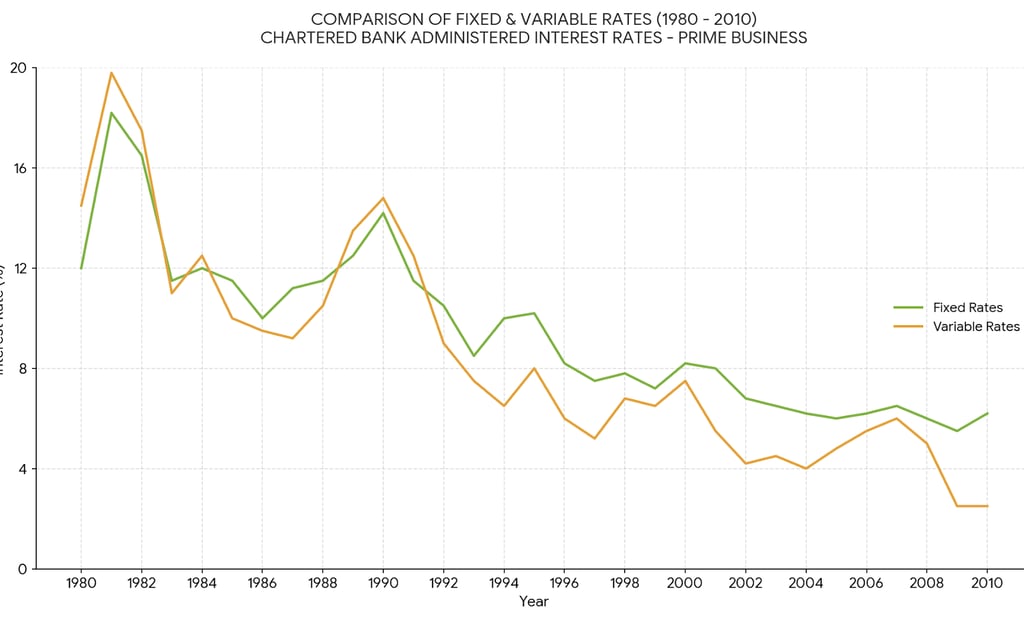

Historical Perspective on Interest Rates

Looking back at interest rate history in Canada, variable rate mortgages have generally been less expensive over time compared to fixed rate options.

There have been periods where variable rates were higher, such as in 1988 and 1989 when speculation and inflation drove rates up significantly. That period marked the beginning of a recession that lasted until 1992.

After 1992, the Canadian government raised rates aggressively, only to reverse course within a year. This pattern of rising and falling rates is part of the economic cycle. Today, many homeowners carry more debt than previous generations, which may lead to slower economic growth and impact how rates change in the coming years.

Understanding these historical patterns can help you make a more informed decision, but no one can predict exactly what rates will do in the future.

Which Option Is Right for You?

The best choice depends on your personal situation:

Consider a Fixed Rate if You:

Prefer stable, predictable payments

Are on a tight budget with little room for payment increases

Want peace of mind during your mortgage term

Believe interest rates will rise significantly

Consider a Variable Rate if You:

Are comfortable with some payment uncertainty

Have flexibility in your budget to handle potential increases

Want to take advantage of lower rates when available

Believe interest rates will stay stable or decrease

How We Can Help

Choosing between fixed and variable rates isn't always straightforward. Paul Mangion and the New Brunswick Mortgage Matters team can review your situation, explain your options, and help you decide which type of mortgage makes the most sense for your needs and goals.

We'll walk you through current rates, show you how different scenarios could play out, and help you make a decision you feel confident about.

Get a Free Evaluation Today

Not sure whether a fixed or variable rate mortgage is right for you? Contact Paul Mangion and the New Brunswick Mortgage Matters team for a free evaluation. We'll help you understand your options and find the mortgage that works best for your situation.

Serving Homeowners Across New Brunswick

We help homeowners choose the right mortgage rate in communities throughout New Brunswick, including:

Fredericton

Moncton

Saint John

Dieppe

Riverview

Quispamsis

Rothesay

And surrounding areas

Start Now

Contact

Reach out anytime for mortgage advice.

Phone

Paul@PaulMangion.com

506-799-0979

© 2026. All rights reserved.

Address : 1191 Lorneville Rd. Saint John,

NB. E2M7G6

NB Brokerage 210053949

NB License 20011866