High-Ratio Mortgage Insurance in New Brunswick

Buying a Home With Less Than 20% Down? Here's What You Need to Know

If you're planning to purchase a home in New Brunswick with a down payment of less than 20%, you'll be required to get mortgage loan insurance. This is known as high-ratio mortgage insurance, and it's an important part of the home buying process that every buyer should understand before they apply for a mortgage.

At New Brunswick Mortgage Matters, we help homebuyers understand all the costs involved in purchasing a home so there are no surprises along the way.

What Is High-Ratio Mortgage Insurance?

High-ratio mortgage insurance protects the lender, not the borrower, in the event that you stop making mortgage payments and there isn't enough money from the sale of the home to cover the outstanding balance.

This insurance is required by law in Canada when your down payment is less than 20% of the purchase price. It is provided by one of three approved insurers in Canada:

CMHC (Canada Mortgage and Housing Corporation)

Sagen (formerly Genworth Canada)

Canada Guaranty

Unlike most types of insurance where you pay a monthly premium, high-ratio mortgage insurance is typically paid as a one-time premium that can be added directly to your mortgage balance.

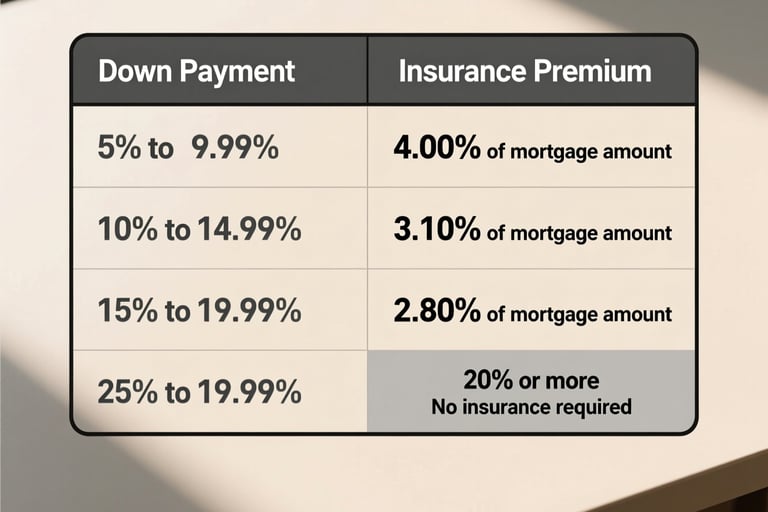

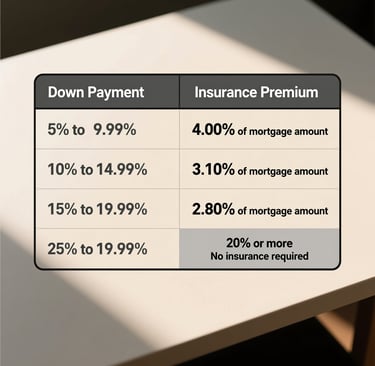

How Much Does Mortgage Insurance Cost?

The premium you pay depends on the size of your down payment relative to the purchase price. The smaller your down payment, the higher the insurance premium.

The key takeaway is simple: the larger your down payment, the less you'll pay in mortgage insurance premiums.

How the Insurance Premium Is Paid

You have two options for paying your mortgage insurance premium:

Pay Upfront

You pay the full premium at closing as an out-of-pocket cost.

Add to Your Mortgage

The premium is added to your mortgage balance and paid off over the life of your mortgage.

If you choose to add the premium to your mortgage, it's important to understand that you'll pay interest on that amount over the full amortization period (typically 25 years). This means the actual total cost of the insurance will be significantly higher than the original premium amount.

How Your Down Payment Affects Your Mortgage

Your down payment amount affects more than just whether you need mortgage insurance. It also impacts:

Your Credit Score Requirements

With a strong credit score, you may qualify for a mortgage with as little as 5% down. If your credit score is lower, lenders will typically require a larger down payment to reduce their risk and the risk to the mortgage insurer.

Your Monthly Payments

A larger down payment means a smaller mortgage balance, which means lower monthly payments.

Your Total Cost of Borrowing

The more you put down, the less you borrow, and the less interest you pay over the life of your mortgage.

Tips for Managing Mortgage Insurance Costs

Here are some practical steps to reduce what you pay in mortgage insurance:

Save for a larger down payment to lower your premium percentage

Maintain a good credit score to qualify with a lower down payment

Pay your bills on time to protect your credit rating

Consider paying the premium upfront rather than adding it to your mortgage to avoid paying interest on it

Work with a mortgage broker to find the best mortgage product for your situation

Why Lenders Require Mortgage Insurance

When a buyer puts less than 20% down, there is a greater risk that if the home needs to be sold due to non-payment, the sale price might not cover the full mortgage balance. Mortgage insurance protects lenders from this shortfall, which is why insured mortgages are also easier for lenders to sell to investors in the financial markets.

What Happens When You Reach 20% Equity?

Once you've built up 20% equity in your home through a combination of your down payment, mortgage payments, and property appreciation, some lenders may still choose to insure your mortgage for their own purposes. However, in these cases the insurance cost is not passed on to you as the borrower.

Get Expert Mortgage Advice Before You Buy

Understanding mortgage insurance is just one piece of the home buying puzzle. Contact Paul Mangion and the New Brunswick Mortgage Matters team today for a free consultation. We'll help you understand all your costs, explore your options, and find strategies to save you money on your home purchase.

Serving Home Buyers Across New Brunswick

We help home buyers understand mortgage insurance and navigate the purchase process in communities throughout New Brunswick, including:

Fredericton

Moncton

Saint John

Dieppe

Riverview

Quispamsis

Rothesay

And surrounding areas

Start Now

Contact

Reach out anytime for mortgage advice.

Phone

Paul@PaulMangion.com

506-799-0979

© 2026. All rights reserved.

Address : 1191 Lorneville Rd. Saint John,

NB. E2M7G6

NB Brokerage 210053949

NB License 20011866